How Much Do Companies Around the World Actually Pay in Corporate Taxes?

by Martin Jacob, Tax Policy Network and IESE Business School

Few economic claims are as politically powerful as the assertion that large companies do not pay their fair share of taxes. Across countries, policymakers and regulators (e.g., OECD, the UK Chancellor, or the European Commission with the European Court of Auditors) as well as NGOs (e.g., Oxfam, the Tax Justice Network, or Greenpeace) regularly argue that firms systematically avoid corporate income taxes, depriving governments of much-needed tax revenues. While these claims are most often directed at U.S. multinationals, similar concerns are voiced in Europe, Asia, and Latin America. But how well does this narrative hold up when confronted with the data?

To move beyond anecdotes, it is useful to focus on effective tax rates (ETRs)—the share of profits firms pay in corporate income taxes—rather than headline statutory rates. Effective tax rates capture what matters economically: taxes paid relative to profits earned, after accounting for deductions, credits, losses, and other features of tax systems.

Using data from more than 18,000 firms across 27 countries over the period 2022–2024, covering major European economies as well as China, India, Japan, Korea, and Brazil, a first basic fact stands out. Across this broad international sample, firms’ effective tax rates are far from negligible. Many firms pay effective rates between 20 and 40 percent, and the average effective tax rate is about 24 percent.

These numbers alone challenge the idea that firms, in general, escape corporate taxation. But they still provide an incomplete picture, as statutory corporate tax rates differ widely across countries. Ireland and Switzerland have corporate tax rates below 15 percent, while Germany, Japan, and Brazil impose corporate tax rates of 30 percent or more. Comparing raw effective tax rates across countries without accounting for these differences risks drawing the wrong conclusions.

A more informative approach is to compare effective tax rates relative to statutory rates. This allows us to assess whether firms pay roughly what the tax code suggests—or whether they consistently manage to pay much less.

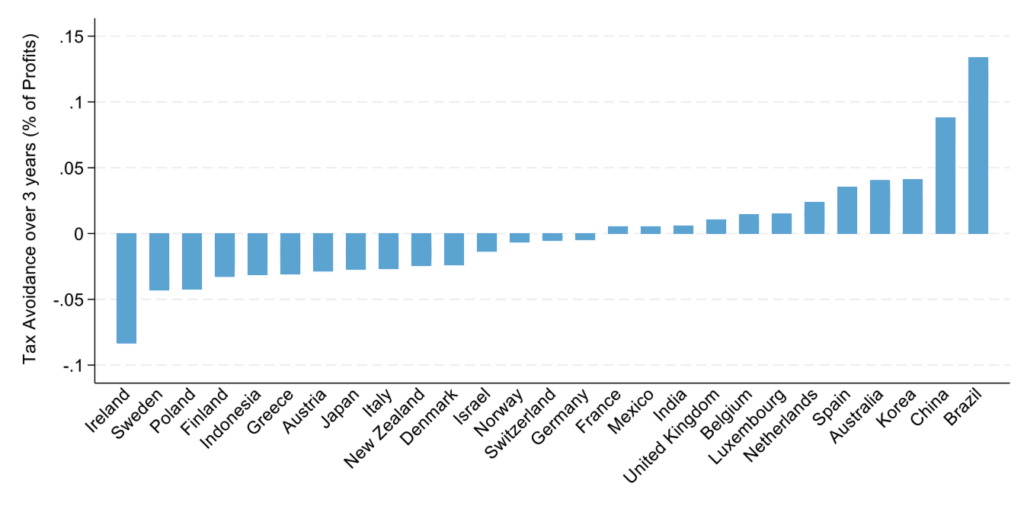

Figure 1 presents this comparison. It shows the gap between the statutory corporate tax rate and the effective tax rate by country. A positive gap indicates that firms pay less than the statutory rate. A negative gap indicates that firms pay more than the statutory tax rate.

Figure 1: Average Effective Tax Tates Relative to Statutory Tax Rates

Source: Compustat and OECD Data Explorer, own calculations

The results are revealing. In most countries, firms on average pay effective tax rates that are very close to statutory rates. This suggests that, at least in aggregate, corporate tax systems in many countries—whether in the European Union, Mexico, India, or Japan—collect what lawmakers intend or even more as in Japan or Italy.

Ireland is a particularly striking case. Despite its reputation as a low-tax jurisdiction, Irish firms pay, on average, more than eight percentage points above the Irish statutory rate. Whatever one thinks of Ireland’s tax model, this is not evidence of widespread tax avoidance. Low statutory rates do not automatically translate into low effective tax burdens.

That said, the data also reveal important exceptions. Two countries stand out: Brazil and China. Brazil has the highest statutory corporate tax rate in the sample, at around 34 percent. Yet firms’ effective tax rates are substantially lower, indicating a large gap between what the tax code prescribes and what firms actually pay. China presents an even more striking pattern. With a statutory rate of 25 percent—squarely in the middle of the international distribution—Chinese firms manage to reduce their effective tax burdens to such an extent that they end up with the lowest average effective tax rates in the entire sample.

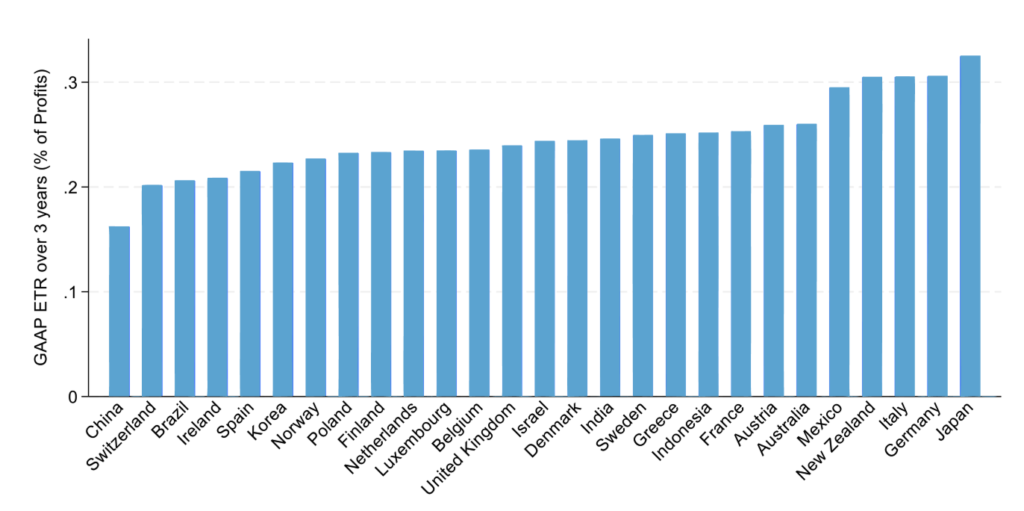

This is illustrated in Figure 2, which shows average effective tax rates by country. Chinese and Brazilian firms, despite operating in jurisdictions with tax rates of 25% and 34%, respectively, pay less in practice than firms headquartered in countries such as Ireland, where the statutory rate is just 12.5 percent.

Figure 2: Average Effective Tax Rates by Country

Source: Compustat, own calculations

These findings matter for policy debates. Claims that firms “do not pay taxes” are made with little reference to actual evidence. The data suggest a more nuanced reality. In most countries, firms pay substantial corporate income taxes and often face effective rates close to—or even above—statutory tax rates. Widespread tax avoidance is not a general feature of the global corporate tax system. However, this does not mean that tax policy concerns should be dismissed. Large gaps between statutory and effective tax rates in countries such as China and Brazil deserve careful scrutiny.

But if the goal is better tax policy, debates should be grounded in empirical facts rather than broad generalizations. Corporate taxation is complex. Simplistic narratives may be politically appealing—but they rarely lead to good policy.

Martin Jacob is Professor of Accounting and Control at IESE Business School.